Looks like you're located outside the continental United States!

While we can't ship Royal NY Line Up boxes to you through our website, our team of coffee traders will be happy to help place your order and secure the best shipping rates for you.

Please note that if you have other items in your cart such as tea or tickets to an event at The lab, you will not be able to proceed to payment until all 22lb. boxes have been removed from your order

Looks like you're located outside the continental United States!

While we can't ship Royal NY Line Up boxes to you through our website, your coffee trader will be happy to help place your order and secure the best shipping rates for you.

The New York arabica coffee market broke down in second-half April, recovered a bit, but has established a bear market since with lower tops and lower lows. Not until the day following First Notice Day for July had the market showed signs of a bottom, actually resembling a reversal days of sorts, albeit over a 2-day period. Since then the market has recovered, but as you can see above, there is formidable resistance over 1.3200 basis September.

London Robusta Market

As you can see above, although London had the same breakdown in late April, it has recovered all those losses and now shows higher highs and higher lows, which is the definition of a Bull Market Trend. Additionally, London has past all resistance but for the contract highs in November of 2016 and January of this year. It will be interesting to see how the tenders in London are taken and what happens to the spot July/Sept spread which was contango on Thursday, June 29th and inverted to backwardation on Friday, June 30th. One last note, on Thursday, June 29th, the London market breached the 200D MA. The last time this market breached the 200DMA to the upside was April of 2016 basis 1550 in the spot month. It crossed back down a year later (April 2017) at 2050.

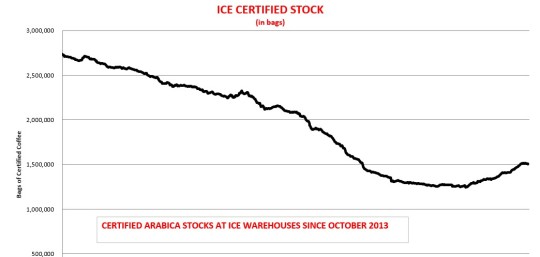

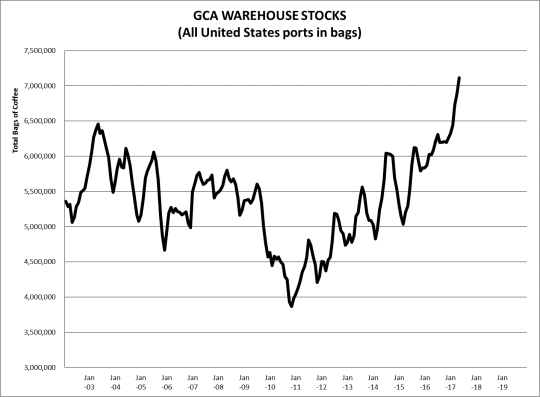

The certified stock numbers (above) have been building since the lows of end 2016/beginning of 2017. The monthly GCA USA stock numbers (below) continue to show us that exporting countries prefer to destock into consuming countries. Total stocks are at their highest levels since 1994.

Macro-Economic Comments:

The Brazilian currency has been pretty much flat since our last report. However, the USD has shown lower tops and lower lows (downtrend). This has added some stability to the global commodity market in general.

We include some brief notes from origin below:

Robustas: Brazil’s Conilon production will be greater year on year. However, not likely enough to cover the Vietnam deficit due to poor weather. Vietnam destocking over the past two seasons has placed the origin in very tight supply. The Jan/March spread has been in backwardization since early May, with all other earlier expiring futures month spreads following suit now.

Brazil: The 2017/2018 crop will be smaller than the prior year. There will be yield issues to consider as well. The more accurate estimates and prognoses for next year’s crop will be determined after the Brazilian winter. Colombians: Colombia’s Mitaca or Fly crop was underwhelming this year. This realization, combined with the erosion of the futures prices, has created wider Colombian premiums. With good weather, the coming year’s main crop should recover. Colombia can once again see a good year for quantity and quality of coffee. Ethiopia: Seeing as though we are at the end of the crop year, offerings are limited to what little remains.

THE BIG QUESTION FOR THE MARKET SHOULD BE: WILL THE SHORTAGE IN AND THE ELEVATED PRICES OF ROBUSTAS DRIVE PEOPLE TO CONSUME MORE ARABICA COFFEE?

If the answer is yes, you may see the rally in robustas temper and an increased value in the NY/London Arbitrage which is at or near life of contract lows.

Once again, this outline is intended to promote thought and an exchange of ideas. If you have an interest to share your point of view, please do not hesitate to contact us.

Good luck and please have a great summer.

*The risk of loss in trading futures and/or options is substantial and each investor and/or trader must consider whether trading is a suitable investment. We do not guarantee that such information is accurate or complete and it should not be relied upon as such.