Looks like you're located outside the continental United States!

While we can't ship Royal NY Line Up boxes to you through our website, our team of coffee traders will be happy to help place your order and secure the best shipping rates for you.

Please note that if you have other items in your cart such as tea or tickets to an event at The lab, you will not be able to proceed to payment until all 22lb. boxes have been removed from your order

Looks like you're located outside the continental United States!

While we can't ship Royal NY Line Up boxes to you through our website, your coffee trader will be happy to help place your order and secure the best shipping rates for you.

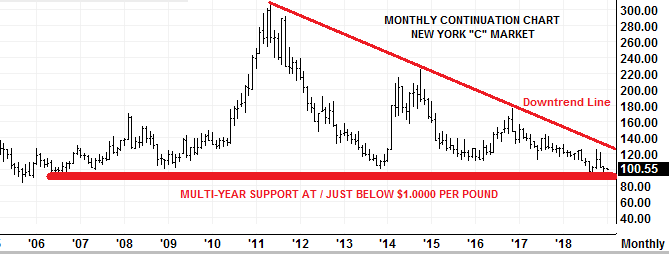

The chart above of course is not much different from our October report, but the differences we can take into consideration give signals for us to factor into our current quarterly report and analysis.

The market had a reversal month in September 2018, which was followed by a 30 cent per pound âcorrectionâ which concluded near the seven-year downtrend line.

As we write, we can report that, for now, the market held the September lows and may be âcoilingâ in advance of another short covering rally.

The year on year Open Interest analysis is much larger (57,000 contracts), which indicates the added âshort interestâ in the market.

The global coffee market has had another three full months to interpret supply and demand projections for the upcoming year. In other words, the downtrend we see is more mature and the interest for producers and/or speculators to hedge or add to existing short positions here at historical lows (near and under $1.00 per pound) is waning.

While the overall long-term trend is lower, one can see on the weekly chart that several downtrend lines have been broken and since the September reversal (with the short cover rally to $1.25), we have yet made a second reversal and can identify a Minor Support Line â which is minor in that it has just been formed. If the market holds these levels, and could break the current downtrend line (at about $1.20), the minor support would then become more significant. If the market could break the last weekly continuation chart high of $1.2550, we would then classify the coffee market as being out of a downtrend and would then be classified as a neutral-trend market.

The daily chart visibly shows us, as the monthly chart does, that the market does not seem to stay at or near $1.00 per pound for very long. We will once again review the points made in our last quarterly report and report the similarities we can make today:

Consider these few factors;

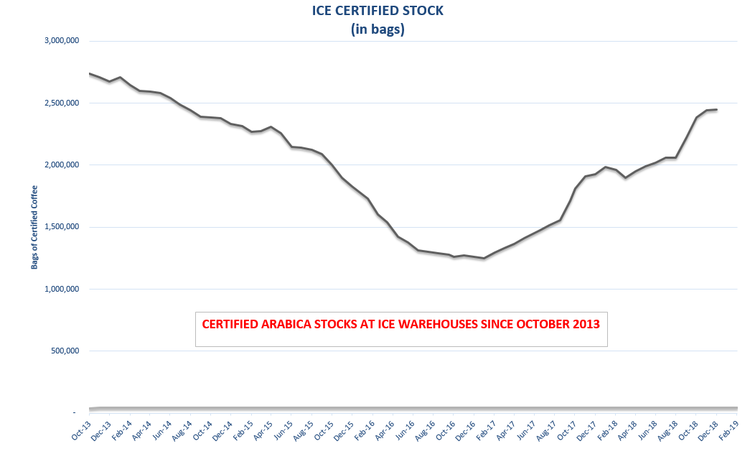

Commitment of Traders had shown the funds and specs short position at record levels of short positions (roughly 105,000 lots). This amount of short position amounts to roughly 26 million bags of coffee for New York âCâ alone. When combined with London, most had expected the number of shorts to have exceeded 35 million bags of coffee. Taking into consideration that position against any surplus in coffee supply, a conclusion could be drawn that the sheer size of such a speculative position would not have been sustainable. For January 2019, we would say that although the open interest and short sided spec position are not of the magnitude we saw in October 2018, the relative factors of this position being hard to sustain still exist. Add that the âmost recent short positionâ had not been reestablished until the market failed $1.20 or $1.15, the house money is much different from last go-around where short positions were very mature and likely established well above $1.50.

Additionally, for some origins (Brazil, robustas, others) we are above cost of production. However, for some source countries, particularly the better mild coffee producers, we were and still remain below COP. We would maintain this train of thought and have seen publications that would validate this conclusion.

Macroeconomic Factors

The Brazilian Real is very influential to coffee prices. Recently, the Real has broken through the 200 DMA to the upside and we may now see a continuation of better prices for the Brazilian currency that we have seen since the end of August.

Source Country Commentary

Brazil

Differentials have remained steady to firm over the past quarter due to the lack of interest from sellers at origin. With Brazil being the largest producer of coffee with the lowest cost of production, cash flow at the farm level allows producers to hold coffee until the time when itâs most advantageous for them to sell. The only way differentials could ease during the remainder of this crop would be a significant rally in the âCâ market. From the availability perspective, the port congestion has experienced relief and the outbound flow of coffee has improved significantly over the last 30 days.

Colombia

Differentials for Colombian coffee remain stable to firm. Export registrations are marginally higher than last year. The mitaca crop seems to be in good shape, although due to lower net prices to farmers, fertilization (or lack of) is a factor. Producers/exporters having been willing sellers of new crop coffee in the September/October futures market rally, now are reluctant to follow prices much beyond $1.1000.

Centrals

Honduras: New crop has been off to a very slow start with 6% of the harvest being exported when normally by this time we would see 15%. Due to the crop being late by almost a month, internal prices for coffee have risen making nearby differentials rise. Compared to last crop, differentials increased due to a combination of the consistently low âCâ market and the delayed crop. With a slight uptick in futures pricing and overall production expected to be approximately 650,000 greater than last year, Honduras is expected to be a more aggressive seller in the coming months compared to other centrals.

Guatemala: Looking for a similar harvest for this year⦠approximately three million 60 kilo bags. Roya is still a concern as the harvest has been under way for a few weeks now with some HB and SHB coffees beginning to ship. Guatemalan producers and suppliers are also looking to sell at fixed prices with concern of the low New York âCâ. Not many are willing to look at selling their coffees on a differential basis. So far quality seems very good and we expect that to stay consistent.

Africa

Ethiopia: The rain in October that continued in to early November helped ripen the cherries. In some areas picking started in November. Early reports from our suppliers indicate that we will have quality which will be on par with years prior if not better. There is the possibility the earlier arrivals will compare nicely to last year due to earlier ripening of cherries and processing underway at origin. We will soon receive pre-shipment and offering samples from Yirgacheffe, Sidamo and also from the Gera Estate in Djimma.

Kenya: Late crop or main crop is well under way as the auction is seeing large volumes of coffees being presented from low quality naturals to high quality cooperative and estate coffees. Production seems to be on par with last year and prices too seem to be firm looking for the highest price at the auction for high-cupping lots. We have just seen our first delivery of cooperative and factory traceable lots as well as a great cupping Organic lot from the late crop. More coffees will start to hit our cupping table as the weeks go on.

Tanzania: Is slowly arriving in the U.S where northern estate lots have been the gems of the season. Over the past few seasons we have seen inconsistency mainly from the southern areas, which seems to be a continued trend overall as well for this year. The port of Dar es Salaam is jammed with coffees from neighboring countries looking to ship their coffees (Burundi, Rwanda, Uganda) and we can expect some delays yet again from this port. This year will be a bit different from prior years where our focus has been more heavily concentrated on traceable, better processed lots from the north near Kilimanjaro and Arusha. Watch for further developments as coffees are starting to arrive from February to April.

Far East and Indonesia

This region can sure use a break from its share of natural disasters. As the Sumatra harvest and exports have started to roll in, we have witnessed fractional relief in the internal market price all while the âCâ market continues to trend lower. Papua New Guinea, Timor, Java, Sulawesi and Bali have all but wrapped up their exports and with the underpinning of the Sumatra so it is our suggestion to insure you have proper coverage into the next six to nine months.

Once again, we reiterate that with the recent lows in the futures markets, our focus here at Royal is aligning ourselves with good supplier-partners who will do their best to maintain quality given the change in prices year on year.

Demand

Roaster interest to extend fixations had diminished during the rally we saw from mid-September to end October. However, the roaster has shown good interest once again as prices dipped through $1.055 and $1.00 on the C futures market. Buyers are now extending price protection beyond six months coverage.

This outline is intended to promote thought and an exchange of ideas. If you have an interest to share your point of view, please do not hesitate to call your sales rep here at Royal, or you could call me.

Looks like you're not logged in! If you have an account, log in here

Don't have an account? Click here to register or close popup window and continue shopping.

You successfully reset your password, please login to your account.

This site uses cookies to allow for proper checkout and order processing; they are not used for any other tracking purposes. By continuing, you accept our use of cookies.