Looks like you're located outside the continental United States!

While we can't ship Royal NY Line Up boxes to you through our website, our team of coffee traders will be happy to help place your order and secure the best shipping rates for you.

Please note that if you have other items in your cart such as tea or tickets to an event at The lab, you will not be able to proceed to payment until all 22lb. boxes have been removed from your order

Looks like you're located outside the continental United States!

While we can't ship Royal NY Line Up boxes to you through our website, your coffee trader will be happy to help place your order and secure the best shipping rates for you.

Your RNY Market Watch, April 2016 update on the coffee futures market.

What’s happening in the coffee futures market

With the operative word “spring”, one can look back at our previous market letter and see how the market has rallied nicely off the double bottom lows in January (1.1335) and March (1.1340).

The New York futures market is now positioned where commodity funds and speculators have exited their previous long term (and profitable) short positions, and have reversed with the rally above the 200 Day Moving Average in mid-March just above 1.2800. The positioning above the 200DMA created 8 cents in added value to the market. It also gave many producers an opportunity to put physical coffee hedges on prior to First Notice Day for May (April 21). As often is the case, an extended move in the market is followed by a corrective pullback. We saw that too, as the market came back to test levels near the 50% retracement for May at 1.2490.

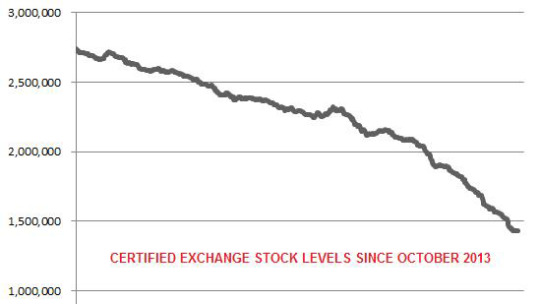

ICE Certified Stocks

Once again, we will also point to the diminishing quantity of certified coffee stock at the exchange. ICE Certified Stocks are now under 1.450 million bags.

There are good reasons to be writing this market letter this week. The Fed Chairperson, Dr. Janet Yellen spoke in New York City this past Tuesday. She made it very clear that while negative interest rates may not be in the cards, she left plenty of room for an expectation of more expansionary monetary policies. This sent the US Dollar to six month lows, helped steady the stock market and should cause commodity prices to appreciate in value against a weaker dollar.

We can see a scenario where currency once again is a major driver of commodity pricing. Not all that much different than it was when we experienced the first tranche of Qualitative Easing (QE1). It may be unreasonable to expect similar monetary activity to that of QE1 or QE2, inclusive of the commodity boom of 2010, but one should be mindful of the power of currency and an active Fed Chairperson.

Origin Notes

In Brazil, the currency has had a very big month. It appreciated in value of about 10%, thanks to impeachment chatter and the aforementioned Fed Speak. This has created good prices for producers and some have taken advantage of this. However, many have stayed to the sidelines in the recent rally of the C contract. Current crop differentials are very much divergent with forward diffs for new crop Brazils.

Colombia has suffered a setback from where they had recovered much market share that passed them by. Due to the impact of El Nino, they are seeing a smaller mitaca crop. It is worth paying close attention to see if normal weather patterns could resume for Colombia.

Centrals have all done well selling this crop and much attention is being paid to the next crop cycle.

Like most origins, Ethiopia had not followed the price decline in the futures market and so, differentials had tightened. With the recent rally in futures, differentials have remained tight.

Once again, this outline is intended to promote thought and an exchange of ideas. If you have an interest to share your point of view, please do not hesitate to call me.

Good luck and please look out for your Royal Coffee New York Salesperson at the SCAA Expo in Atlanta, April 14 to 17 at Booth 1013.